Transparency International Sri Lanka’s (TISL) report on ‘Transparency in Corporate Reporting’ poses the question of whether corporate entities disclose information to stake-

holders optimally, beyond their mini- mum statutory obligations.

Indeed, Transparency International’s (TI) interest in the corporate sector helped establish the Transparency in Corporate Reporting (TRAC) assessment methodology, which has been imple- mented in Sri Lanka.

TISL has for the first time conducted a TRAC report assessing the corporate reporting practices of Sri Lanka’s top 50 listed entities (by market capitalisation at 28 February 2019).

This assessment scores companies on their 2018 or 2018/19 annual reports (and any other publicly disclosed material) across three thematic sections broken down into 26 questions ranging from stated policies on facilitation payments to disclosure on corporate holding struc- tures. These scores are aggregated and companies ranked to illustrate the perfor- mance of the top 50 listed entities.

TISL notes that the report presents “an opportunity to take stock of current dis- closure practices with a view to starting a conversation on potential innovations for the future. A low rank is not a sign of wrongdoing but rather, highlights a potential opportunity to enhance disclo- sure to stakeholders.”

“Whilst we appreciate that senior man- agement cannot oversee every individual action within an organisation, our method- ology does assess the stated commitments of management to tackle corruption and improve transparency. We acknowledge from the outset that there will always be differences in organisational culture and policy implementation, which falls beyond the scope of this report,” it adds.

The TRAC assessment analyses a com- pany’s reporting practices through pub- licly available information in three areas that are crucial to fighting corruption: their anticorruption mitigation proce- dures, transparency in reporting on their organisational structure, and the key financial data disclosed on their national and transnational operations.

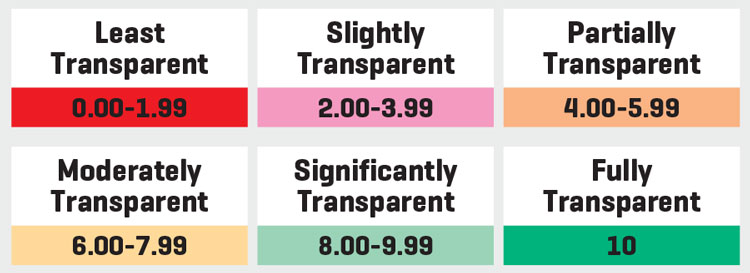

Overall, company scores range from zero to 10 where zero is the least trans- parent in corporate reporting and 10 is fully transparent.

As for the ‘why’ of it all, TISL says: “From bribery scandals to tax avoidance, companies are under increasing pressure to account for their actions around the world. Similarly, the corporate sector can be a leader in driving improved standards of corporate governance. Transparency is crucial for ensuring that companies are accountable for their activities, enabling the prevention, detection and prosecution of corrupt practices.”

It maintains that “one important out- come of conducting this review is to ensure that senior management, where necessary, incorporates and strengthens already existing anticorruption practices in their companies, and makes this infor- mation publicly available.”

The companies are equally scored in three thematic sections: reporting on anticorruption programmes, organisational transparency and domestic financial reporting; the final TRAC score for each company is given by taking the average of the three thematic scores and then rebasing the scores on a scale from zero to 10.

They are then ranked from number one to 50 based on their overall scores. Companies with equal index scores were ranked equally and ordered alphabetically.

As for the report’s findings, the average top 50 listed company in Sri Lanka is moderately transparent with a score of 6.73.

Only five companies (John Keells Holdings, Seylan Bank, Hemas Holdings, National Development Bank and People’s Leasing & Finance) are classified as significantly transparent. All the companies are at the very least, partially transparent with the lowest score being 4.33.

Companies were slightly transparent in reporting on their anti- corruption programmes with an average score of 27 percent; companies had significant organisational transparency with an average score of 86 percent; and 31 companies were fully trans- parent in domestic financial reporting with the average score across all 50 companies being 92 percent.

Although the average top 50 company is moderately trans- parent, on average, companies have scored poorly in terms of their reporting on anticorruption programmes.

TISL recommends that companies develop a comprehensive anticorruption programme and make the policy that forms the basis for it publicly available; provide anticorruption training for employees including senior management and directors; establish a whistleblower policy that incorporates anonymity and ensures a channel for two-way communication with them; and explicitly prohibit facilitation payments or any other pay- ments that may be construed as a bribe.

It calls for extending the anticorruption policy or code of con- duct to persons who are not employees but are authorised to act on behalf of the company or represent it; publicly disclosing any commitment to anticorruption and compliance with laws in Sri Lanka and other countries of operation; extending the anticorruption policy or code of conduct to non-controlled per- sons or entities that provide goods or services under contract; and publicly stating company policy on political contributions. In terms of organisational transparency, TISL recommends that companies clearly categorise and list any fully consolidat- ed subsidiaries and non-fully consolidated holdings irrespec- tive of materiality; and explicitly state countries of incorpora- tion, and operation of fully consolidated subsidiaries and non-

fully consolidated holdings.

Publicly disclosing the amount spent and description of any community or charitable contributions is recommended for domestic financial reporting, as is publishing data on revenue, capital expenditure, pre-tax income, income tax and communi- ty contributions for all foreign operations vis-à-vis country by country reporting.